Equity outlook: Time for quality and growth again

- 25 July 2022 (7 min read)

- With increasing economic uncertainty, we believe investors should focus on high-quality stocks demonstrating earnings resilience and strong earnings growth

- We believe valuations for the ‘best’ growth and ‘highest-quality’ companies are back to sustainable levels and bond yields have likely peaked

- The need to invest in digital, automation and net zero technologies are key secular drivers

- A return to higher premiums on growth would underpin outperformance of those stocks

Investors have endured a tumultuous period during the first half of 2022 in the wake of higher bond yields and declining equity valuations. The tightening of monetary policy in response to the inflation shock and the subsequent consequences for growth have encapsulated the key macro narrative.

High government bond yields have forced a decline in price-to-earnings ratios and there are now increased concerns about corporate earnings growth falling short of what is currently suggested by consensus forecasts.

Year to date, the MSCI World NR and JP Morgan Global Government Bond indices are down by 21% and 15% respectively.1

As such, investors are understandably concerned what the coming quarters will bring and what a peak in bond yields and more reasonable equity valuations could mean for market returns going forward.

But given what is likely to be a more challenging period for earnings growth, we believe investors’ focus should be on high-quality stocks which can demonstrate earnings resilience and strong earnings growth.

The rise in real bond yields from the end of 2021 has coincided with a drop in global equity prices and an underperformance of Growth stocks, relative to Value. This has been the opposite of what happened in 2020 when real yields fell in response to the COVID-19 outbreak and the further easing of monetary policy.

Rising bond yields have closed the relative yield gap between bond and equities and dramatically impacted ‘long duration’ parts of the equity market, i.e., companies with high earnings growth, which are most sensitive to changes in the discount rate.

In a note published earlier this year we looked in detail at the relationship between bond yields and equities as well as the relative performance of Growth versus Value in a rising yield environment.

Equity opportunities

The historical relationship between real bond yields and equity valuations is well documented. In recent weeks, bond yields appear to have peaked, with markets having priced in the idea the Federal Reserve will take US interest rates to around 3% in this cycle. We would argue the valuations of Growth and Quality equities are now consistent with the current level of real yields – it has been a dramatic adjustment.

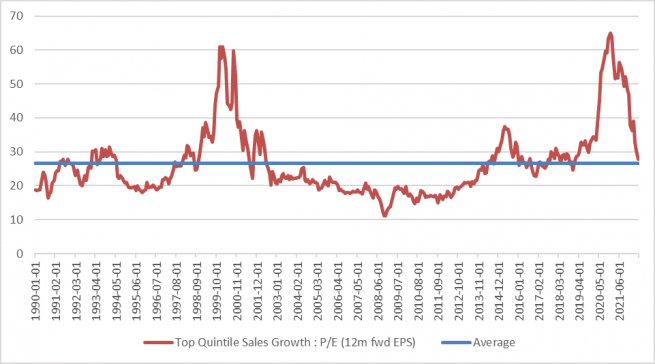

Taking the top 20% of companies with the strongest sales growth in the global equity universe, the price-to-earnings ratio has dropped from around 48 times to below 27 as of July (see chart below).2 The adjustment in the multiples of quality stocks – defined by return on equity – has also fallen sharply.

- RmFjdFNldCBhcyBvZiAxNCBKdWx5IDIwMjI=

- QVhBIElNLCBKdWx5IDIwMjI=

In our view, valuations for the ‘best’ Growth and highest-quality companies are now back to pre-pandemic levels. While they are not cheap – and these parts of the market became very expensive in 2020 and 2021 – they are, however, now at more attractive levels. Furthermore, in a more challenging environment for global GDP growth, we see little reason why real yields should rise further from current levels. There is a reasonable argument then that most of the valuation adjustment has already taken place and the focus should now shift towards earnings delivery and growth.

What we have witnessed globally is also evident in Europe where multiples have fallen sharply. Bond yields have risen from their 2021 lows and Growth and Quality companies have underperformed. While the economic outlook is complicated for Europe, given the proximity of the war in Ukraine and the disruption to energy markets, we don’t see real bond yields moving higher from current levels. In both the US and Europe, real yields are back to pre-COVID-19 levels, and in terms of their impact on equity valuations, we believe the worst is likely over. Where this has been the worst is in the Growth and Quality parts of the market.

A potential re-rotation

The underperformance of Growth contrasts markedly with the outperformance of Value stocks. This rotation has several aspects to it. First, Value stocks were cheaper than normal during 2021 and going into the start of this year. Growth outperformed Value during the early stages of the pandemic and during the second half of 2021.

A reversal was always likely once interest rate expectations started to rise as relative valuations had become out of line with historical norms. Secondly, typical cyclical sectors saw a rapid improvement in earnings as the global economic recovery from the pandemic accelerated in 2021 and early this year.

From a sector point of view there has been differential performance in a falling overall market. Taking the S&P 500 universe, the Financials, Utilities and Consumer Staples sectors have fallen less than the market overall on a year-to-date basis while the Energy sector has delivered a positive return.3

Financials have performed well given the backdrop of very low interest rates in 2020-2021 and buoyant capital market and lending activity. Energy stocks have been boosted by windfall earnings from the rise in global energy prices.

In 2022 the sectors in the US equity market which have experienced the most negative changes in price-to-earnings ratios include Information Technology, Consumer Discretionary and Consumer Services, while more value-like sectors such as Utilities, Consumer Staples, parts of the Pharmaceutical sector and Energy have seen little adjustment in multiples (less than the broad market) and limited downward revisions to forward earnings.

The net effect, which has been well documented, is that Value outperformed Growth in the first half of 2022 in a falling market because Value stocks de-rated, on average, less than Growth stocks.

The valuation adjustment, combined with global bond yields having potentially reached a peak, suggests the underperformance of Growth and Quality could potentially reverse going forward. Comparing current forward price-to-earnings ratios with consensus earnings growth forecasts suggests sectors like Consumer Staples, Financials, Healthcare and Utilities are expensive in aggregate.

For Technology this ratio is now almost back to its long-term average even with the sector already having seen some significant downgrades to earnings growth forecasts in recent months.

The broader market dynamics have meant popular stocks in the technology and consumer services sectors have disappointed investors this year. The NASDAQ Composite index – dominated by companies in these sectors – is down 28% year to date and around 30% since its peak.4

Squeezed consumer real incomes have led to questions over the amount of spend able to be devoted to activities like online entertainment and new digital devices and services.

However, in our view, these concerns are likely to be temporary. The top 10 companies in terms of market capitalisation in the NASDAQ index have seen significant multiple contraction from their peak 2021 price-to-earnings ratio while one-year forward earnings forecasts are positive.

We believe the higher-than-market valuations are justified by long-term resilient growth performance. Some specific stock examples here would include PayPal, Adobe, Salesforce, and Apple.5

All these examples currently have an estimated price-earnings ratio close to or lower than was the case in February 2020 and have meanwhile delivered earnings growth.

Forecasts holding up

At a broad market level, earnings forecasts have yet to undergo significant downward adjustments. However, for cyclical companies this will occur as GDP growth slows.

The momentum of earnings forecasts has deteriorated – meaning there have been more downward revisions to earnings-per-share (EPS) estimates – but the aggregate growth rate for the next 12 months remains at 9% for the MSCI World Index (9.5% for the S&P500 and 7.6% for the EuroStoxx universe).6

Typically, in a slow or recessionary environment, earnings growth turns negative. In the 2009 recession, global equity earnings fell by up to 40% and by around 20% in the COVID-19 downturn.7

For all major equity markets, the consensus forecast is for aggregate EPS to show growth in both 2023 and 2024.

Equity analysts rarely predict negative earnings growth, but it does happen. Generally, such periods see investors willing to pay a higher multiple for those companies that do manage to sustain growth.

If major economies are going to go through a normal business cycle slowdown in response to central banks trying to bring down inflation, then more cyclical parts of the equity market are likely to suffer while there will be little reason to take multiples on typically defensive sectors even higher.

Lower bond yields in anticipation of slower growth and lower inflation will also help longer-duration growth equities.

The main risk is that earnings overall will fall if the global economy weakens. Previous recessions have seen aggregate earnings fall anywhere between 20% and 40% from peak to trough. However, most at risk are sectors that have seen strong earnings growth in the cyclical recovery from the pandemic.

The key point is that when growth becomes scarcer at the overall market level, companies that have the most resilient earnings profiles and have delivered stable and strong earnings growth in the past should attract more of a premium relative to the market. In which case, the de-rating of Growth companies may already be sufficient.

Earnings focus

There are secular reasons to be more positive on growth stocks as well. The pandemic-driven disruptions have highlighted the need to accelerate investment in technology and to respond to higher labour costs through automation.

The success of biotechnology companies in rapidly developing COVID-19 vaccines and the promise of extending the use of innovative technologies to more healthcare applications suggests, in our view, a potentially strong earnings outlook for that sector in coming years.

Areas such as online healthcare and robotic surgery are key developments in the broader healthcare space showcasing the role that digitalisation and automation can bring to delivery of consumer services.

Let’s not ignore either the momentum behind moving to a net zero carbon economy in the years ahead, with growing amounts of investment in new technologies and electrification across agriculture and multiple industrial sectors.

These trends support a long-term thematic approach to equity investing which is dominated by companies with superior growth trajectories, strong returns to equity and limited debt.

- UyZhbXA7UCBkYXRhIC8gQmxvb21iZXJnLCBKdWx5IDIwMjI=

- RmFjdFNldCAvQmxvb21iZXJnIDE0IEp1bHk=

- Rm9yIGlsbHVzdHJhdGl2ZSBwdXJwb3NlcyBvbmx5OyBzdG9jayBtZW50aW9ucyBzaG91bGQgbm90IGJlIHZpZXdlZCBhcyByZWNvbW1lbmRhdGlvbnM=

- Qmxvb21iZXJnIEp1bHkgMjAyMg==

- Qmxvb21iZXJnL0lCRVM=

Sectors that have performed well during the Value outperformance period have seen a significant upturn in earnings. These are sectors that tend to have very a significant cyclical component to the evolution of earnings over time. The Energy, Financials, Materials, and broader Industrials sectors have seen a dramatic growth in average earnings per share over the last year, as was estimated by the Institutional Brokers' Estimate System. For example, the growth in trailing 12-month earnings-per-share for the S&P500 Energy sector was 370% to July 2022. For Industrials, growth was 47% and for Materials it was 43.5%. These growth rates are not sustainable and EPS levels are likely, in our view, at cyclical peaks (see charts 2 and 3).

As the table below shows, the earnings picture is changing. From a Growth/Value point of view, this year has been strong for Value given what we have seen in sectors like Energy and Materials. However, going forward earnings in the Growth style are expected to be stronger. This is consistent with better quality long-term earnings performance from the growth parts of the equity market. There is no guarantee, but this should be reflected in total return performance.

| EPS Growth Forecast | 2022 | 2023 | 2024 |

| MSCI US Value | 14.5% | 7.2% | 6.9% |

| MSCI Growth | 5.3% | 10.7% | 10.6% |

(Source: IBES, S&P, Refinitiv, July 2022)

Historically, earnings growth has been less volatile in sectors such as Information Technology, Healthcare and some Consumer Services companies. Stocks in these sectors have demonstrated strong earnings growth with limited cyclicality. This justifies a higher premium.

The gap between the price-earnings ratio of Technology and that of the market overall and of the more cyclical sectors such as Industrials and Financials has come down over the last year to a level that we think is more justified.

At the sector level, the 12-month forward price-earnings ratio for Consumer Services (a sector that includes stocks like Amazon, Alphabet, Netflix, Meta Platforms, Comcast, and Walt Disney) is now below that of the overall S&P500.

The macroeconomic outlook is challenging – we are yet to see a peak in global inflation, or any easing of the disruption to global energy and food markets which has resulted from the Ukraine crisis.

However, markets have significantly corrected and the rotation away from Growth to Value in the past 12 months has created the opportunity to think about adjusting equity exposure in anticipation of a recovery period.

Companies with a proven track record of delivering earnings and at the forefront of technological innovation should again demand a ratings premium, especially when the broader earnings environment faces challenges.

At the macro level we believe a peak in bond yields should prevent any further de-rating of good quality companies with solid earnings growth.

- VGhlIGluZm9ybWF0aW9uIGhhcyBiZWVuIGVzdGFibGlzaGVkIG9uIHRoZSBiYXNpcyBvZiBkYXRhLCBwcm9qZWN0aW9ucywgZm9yZWNhc3RzLCBhbnRpY2lwYXRpb25zIGFuZCBoeXBvdGhlc2lzIHdoaWNoIGFyZSBzdWJqZWN0aXZlLiBUaGlzIGFuYWx5c2lzIGFuZCBjb25jbHVzaW9ucyBhcmUgdGhlIGV4cHJlc3Npb24gb2YgYW4gb3BpbmlvbiwgYmFzZWQgb24gYXZhaWxhYmxlIGRhdGEgYXQgYSBzcGVjaWZpYyBkYXRlLiBEdWUgdG8gdGhlIHN1YmplY3RpdmUgYXNwZWN0IG9mIHRoZXNlIGFuYWx5c2VzLCB0aGUgZWZmZWN0aXZlIGV2b2x1dGlvbiBvZiB0aGUgZWNvbm9taWMgdmFyaWFibGVzIGFuZCB2YWx1ZXMgb2YgdGhlIGZpbmFuY2lhbCBtYXJrZXRzIGNvdWxkIGJlIHNpZ25pZmljYW50bHkgZGlmZmVyZW50IGZvciB0aGUgcHJvamVjdGlvbnMsIGZvcmVjYXN0LCBhbnRpY2lwYXRpb25zIGFuZCBoeXBvdGhlc2lzIHdoaWNoIGFyZSBjb21tdW5pY2F0ZWQgaW4gdGhpcyBtYXRlcmlhbC4=

Companies shown are for illustrative purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.