Eurozone – Difficult roads ahead

- 13 December 2022 (5 min read)

Key points

- We expect Eurozone GDP to contract by 1% between Q4 2022 and Q1 2023, followed by a weak recovery

- Limited labor market ramifications imply persistent (core) inflationary pressures

- We forecast ECB deposit facility rate (DFR) to peak at 2.5% next March and an initial gradual partial APP unwind from next April

- Markets have yet to fully grasp public debt sustainability issues

Growth’s swan song

Eurozone GDP grew by 0.2% quarter-on-quarter in Q3 2022, remaining resilient despite increasingly alarming forward-looking surveys. We think this resilience is mainly due to three factors: ongoing positive impetus from COVID-19 reopening, resulting in a swifter-than-expected convergence to more normal savings behaviour and strength of gross disposable income underpinned by a strong labor market.

Amid a highly uncertain macro environment, we think a grim outlook lies ahead. Constrained energy supply and faltering demand are likely to push the Eurozone into a marked recession this winter while a changing economic structure and tight monetary policy will lead to a sub-par recovery. Monetary policy dominance will generate increasing worries about public debt sustainability, while the future of European Union (EU) fiscal rules and the Next GenerationEU (NGEU) package are likely to bring additional political and policy challenges.

An inevitable recession

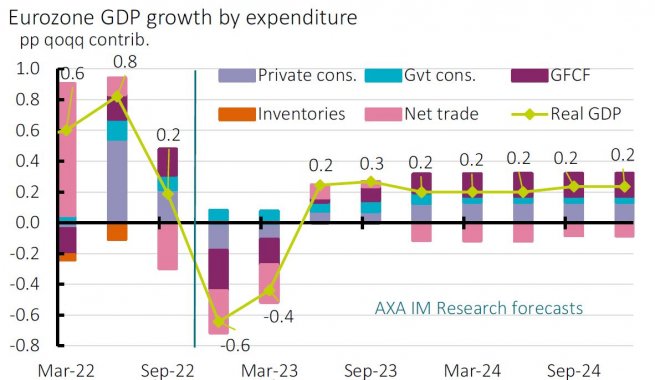

We have revised up our GDP forecasts slightly, though continue to project the Eurozone economy will contract led by energy (gas) supply constraints (and/or elevated prices) and weakening demand from a historic terms-of-trade shock. However, higher levels of gas storage during a warmer autumn mean severe output disruptions are less likely. We now expect Eurozone GDP to contract by 1% (from -1.4% previously) between Q4 and Q1 2023 where both domestic demand and net trade are likely to contribute in tandem (Exhibit 6).

Although Germany is making good progress shifting its energy mix away from Russia, the latest data confirms our initial assessment that it is likely to be the most affected of the large Eurozone countries1 . But indirect (trade) effects imply other countries are unlikely to escape contraction.

A weak recovery

We think the recovery will feature three key characteristics. First, the seasonal nature of the supply disruption implies that when capacity comes back online, it will swiftly translate into a bounce in economic activity – whether to fulfil demand or for stock building purposes. This is likely sooner rather than later in Germany, thanks to the implementation of energy price caps from March and an expected China pick-up, as shown by a positive net trade contribution to growth (Exhibit 6).

- UGFnZSwgRC4sIExlIERhbWFueSwgSC4sIENhYmF1LCBGLiwgVG9wYS1TZXJyeSBJLiBhbmQgQWRlZ2JlbWJvLCBNLiwg4oCcVGhlIGVjb25vbWljIGltcGFjdCBvZiBhIFJ1c3NpYW4gZ2FzIGN1dC1vZmbigJ0sIEFYQSBJTSBNYWNybyBSZXNlYXJjaCwgMzAgU2VwdCAyMDIy

Second, the seasonal nature of the shock coupled with supportive fiscal policy should avoid a full economic cycle adjustment. In other words, we expect only a limited 0.7 percentage point (ppt) unemployment rate rise to 7.2% in late 2023 enabling demand to recover modestly, especially when inflation softens while wage growth accelerates. Our models suggest that negotiated pay growth (excluding bonuses) will reach around 4.5% year-on-year from Q2 2023 and surpass inflation which will recede to 2.5% in Q4 23, mainly owing to negative base effects from energy (more below). Furthermore, the NGEU should is likely to support investment despite tight monetary policy, which will keep the recovery pace below potential.

Third, mending the supply side of the economy – changing the energy mix (especially for Germany) and securing supply chains –is a process that will likely take years. While uncertainty runs high, we think the quantum and/or price adjustment will result in a permanent supply shock. The European Commission has estimated Eurozone real potential growth between 1.1% and 1.2% since 2015 on average, consistent with a 0.3% quarterly growth rate. Reflecting the persistent constraints the economy will face, we have pencilled in 0.22% quarter-on-quarter on a sequential basis through 2024. We do not expect the Q3 2022 GDP level to be recouped until Q2 2024.

No swift end in sight for ECB’s hawkish bias

We continue to project headline and core inflation to peak in Q4 2022 at 10.8% and 5% (annual) respectively. The former is poised to recede swiftly owing to negative energy base effects, fiscal measures and an increased inability to pass through input costs as demand falters this winter. We project headline inflation to drop by around 2ppt year-on-year each quarter, ending 2023 at 2.5%, consistent with a 5.6% annual average next year (8.6% this year). In 2024, an unwind of fiscal measures and likely persistent issues with supply will push energy prices moderately higher, to a 2.4% headline average.

We project a more moderate core inflation retracement of c. 0.6ppt on average for each quarter of next year, mainly coming from non-energy industrial goods, while services are likely to prove much more sticky owing to the staggered nature of wage negotiations and the expected resilience of the labor market. All in, we project euro area core inflation to average 3.8% next year, only 0.1ppt lower than this year, and stabilizing above the ECB medium term inflation target at 2.3% in 2024 (Exhibit 7).

The ECB raised its DFR by 200 basis points (bps) in just three meetings this year, to 1.5%. We, and the market, expect an additional 50bp rate hike in December. With inflation expected to fall and policy moving towards restrictive territory, frontloading is likely behind us, but it does not mean an end to hawkishness altogether. We think the ECB is likely to shift to 25bp increases in February and in March to reach 2.5%, which would be some way below the peak rate the market is pricing of 2.9% in mid-2023 – yet still in restrictive territory.

The ECB’s policy focus is likely to switch to Asset Purchase Programme (APP) unwind next year. Prior to high level guidelines to be communicated at the December meeting, we think the ECB is unlikely to make a concrete decision on a path before its March 2023 meeting at the earliest. We expect gradual, partial reinvestment, before picking up the pace towards year-end, mindful of already high sovereign funding rates, high public indebtedness and record expected net issuance next year. Although peripheral bond spreads have behaved well so far, we caution against complacency.

Crunch times for Eurozone ahead

The past decade of falling interest rates has allowed the Italian debt management office to lower the implicit interest rate on public debt to 2.4% in 2021, maintaining debt maturity to seven years while Italian public debt jumped to 151% of GDP in 2021. Thus, there are some strong firewalls against public debt trajectory rising uncontrollably within the next couple of years, including the fiscally conservative first steps of the new government. A continuously decreasing share of non-resident bond holders (under 30%) has likely also helped limit market pressure so far.

However, we think there is likely increased market stress ahead. First, there is a clear risk of public deficits overshooting next year owing to optimistic government growth forecasts and the possible need to extend energy measures. Second, the Italian government has yet to implement any of its electoral pledges (worth 2%-4% of GDP). Third, our baseline forecasts are consistent with a primary surplus worth 2.1% of GDP to stabilise the public debt-to-GDP ratio in 2024 – a high bar. Fourth, although gradual, the ECB’s unwind of the APP would reduce its high share of holdings (26%). Finally, there are significant challenges to reaching an agreement on future fiscal rules after the EC issued initial guidelines, which could be detrimental to fiscal credibility.

After general elections in Greece, Finland and Spain next year, the European Parliament will be up for renewal in spring 2024. By then, we will have more experience of enhanced mutualised debt in Europe with NGEU in the last third of its expected life. Alongside heightened market pressure from challenging public debt trajectories, EU institutions will likely face a renewed crunch time amid ever-polarised voters.

The information has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. This analysis and conclusions are the expression of an opinion, based on available data at a specific date. Due to the subjective aspect of these analyses, the effective evolution of the economic variables and values of the financial markets could be significantly different for the projections, forecast, anticipations and hypothesis which are communicated in this material.

Our views for 2023

Read our full outlook to find out more about our experts' views.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.