US reaction: Inventory leads to another surprise drop in Q2 GDP

- 03 August 2022 (5 min read)

Key points:

- GDP contracted by 0.9% (saar) in Q2, worse than our +1.0% forecast and consensuses +0.5%.

- Two quarters of contraction marks a technical recession in most economies, but the US dates recessions according to an assessment by the NBER.

- Once again, a sharp fall in inventory was accredited for the decline in GDP, although investment spending was also dragged lower through residential investment.

- Today’s reading lowers our GDP outlook from 1.9% for the year as a whole – mechanically to 1.5% – although further detail on the composition of Q2 GDP growth will be necessary to fine tune the view.

- We persist with our outlook for the Fed to hike by just another 75bps (50bps in September and 25bps in October) to a peak of 3.25%.

The US economy surprisingly contracted in Q2 by 0.9% (saar). This was much weaker than our forecast for a rise of 1.0% and reflects the impact of another sharp slowdown in inventory growth. Given the evolution of estimates of growth across Q1, we are reluctant to put too much weight on the current breakdown. That said, the growth outlook should now be lower than the 1.9% we had forecast for 2022 as a whole. Moreover, although two quarters of negative growth constitutes a technical recession in most economies, the US dates recessions according to a deeper analysis by the NBER. With domestic and final domestic demand growth both falling this quarter, the US is closer to recession than we had considered.

US GDP contracted again in Q2, down 0.9% annualized, compared with consensus forecasts of +0.5% and our own outlook for a modestly firmer 1.0%. This time the Atlanta GDP now tracker was closer, which suggested a fall of 1.2%. The drop marks the second successive quarterly contraction and would constitute a technical recession in other parts of the world. In the US, the NBER determines the dating of recessions, determined by an assessment of declines in a broad range of sectors. With declines in domestic demand and domestic final sales, there is more of an argument for suggesting weakness began in Q2, but the broad strength of the labor market still questions outright recession – despite signs of further weakening again in today’s initial jobless claims and in June’s household measure of employment, this will need ongoing monitoring.

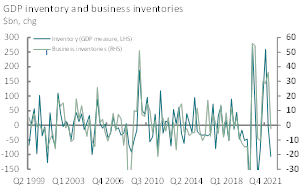

The surprise drop today reflected a weaker outturn in investment spending and in the very volatile inventory component. Total investment spending recorded a drop of 4.0% (saar), twice as sharp as we had expected. Business investment recorded -0.1% on the quarter – basically flat, following a strong 10% rise the previous quarter. However, residential investment fell by 14%, catching up with the recent sharp decline in sales (Exhibit 2). Together investment reduced the GDP outlook by around 0.5% ppt (saar). Inventory once again accounted for the biggest surprise, inventory is judged to have fallen much more sharply than underlying industry trackers suggested (Exhibit 1) and alone accounted for a 2.0ppt shortfall in GDP relative to our forecast. We are cautious of reading too much into this at this stage. This was also the initial explanation for the decline in Q1 GDP, but subsequent revisions went on to revise the consumer spending element lower and inventory was revised higher. Consumer spending rose by 1% on the quarter, exactly in line with our forecast. Net trade made up the difference, contributing nearly 1% more than we had forecast, with exports rising by a sharp 17% on the quarter, while imports posted a more restrained 3% leading to the biggest net trade boost since Q2 2009.

With Q2 GDP falling short of our expectations the outlook for 2022 growth has fallen further. Mechanically replacing today’s drop with our forecast would reduce our GDP outlook to 1.5% for the year as a whole (from 1.9%). Consensus is, for now, at 2.0%. However, we will await a further evolution in the data before revising our forecast. If inventory continues to be seen as the main culprit for Q2’s contraction, then Q3 could be firmer then we had previously considered. However, if Q1’s pattern is repeated and an initial inventory drop is later revised in to a further slowing of household or business investment spending, then this may suggest weaker momentum that could lower our outlook. With the US having fulfilled most countries definition of a technical recession, the probability of full-blown recession in the US is evidently much closer.

Fed Chair Powell last night stated that he had not seen today’s GDP print but warned that first estimates could be misleading and were often revised. He did not want to be drawn on the outlook for recession. The underlying softening in economic activity has been evident in the US for the last several months and has more recently led markets to consider the Fed’s reaction to a weakening economy. In part, this depends on the path of inflation. Powell stated that a slowdown in the economy to below potential was necessary to restore price stability. This is now clearly in train, but we remain to see how quickly this feeds through to the labor market and prices. For now, we continue to expect the Fed to hike by 50bps in September and again by 0.25% in October, but to leave rates on hold at 3.25% in December.

Markets reacted to the disappointing GDP figure by easing rate expectations. The outlook for the end year Fed Funds Rate fell below 3.25% for the first time since the Fed’s hawkish tilt in mid-June. Term rates also fell, the 2-year and 10-year Treasury yields dropping 12bps each to 2.84% and 2.66% respectively. The dollar also retreated by 0.5% against a broad basket of currencies.

Exhibit 1 - Inventory sees exaggerated fall again

Exhibit 2 - Residential investment catches up with housing

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.