China green bonds: Seeking harmonisation in a sector that could boost the climate change fight

- 07 July 2021 (5 min read)

As part of AXA IM’s commitment to fighting climate change, we aim to be a leading investor in the green bond market. We have already put to work more than €10bn in green bonds1 and we want to continue supporting and improving an asset class that, we believe, can be a crucial part of the world’s ambition to reduce emissions and limit global warming. As part of this, we see a major role for Chinese green bond issuance and consider the sector to be a great opportunity to widen our investment universe.

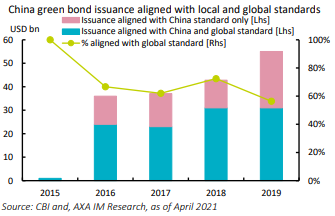

The Chinese green bond market has grown rapidly since its debut in late 2015. It is a similar trend to that we have seen for the green bond market globally, and China has quickly become the world’s largest issuer of green bonds and second largest market in terms of issuance volume. We believe that this momentum is very likely to continue over the medium term – especially as green bonds represent an important tool for Beijing to achieve its 2060 carbon neutrality objective2 .

Figure 1: Rapid growth in China green bond issuance

From an analytical and evaluation perspective, we believe that assessing the quality and credibility of Chinese onshore green bonds is a quite different exercise than for green bonds from other geographies. First, because green bond standards and practices in China differ from those used globally. Second, because onshore issuances in China may miss some of the key elements and criteria that we use in the AXA IM’s green bond assessment framework3 to conduct a proper, comprehensive analysis.

We are looking to establish strong and constructive relationships with Chinese issuers and underwriting banks, to make sure that our expectations for green bonds are well understood. We are also closely working with our Asia-based colleagues to ensure that our analysis is properly conducted, and in a timely manner – despite time zone and language issues. Our research highlights that there is a need for:

- Harmonisation of Chinese and global green bond standards

- Improved dialogue and transparency between Chinese issuers and investors

- Establishment and disclosure of a clear sustainability strategy and objectives from Chinese green bond issuers

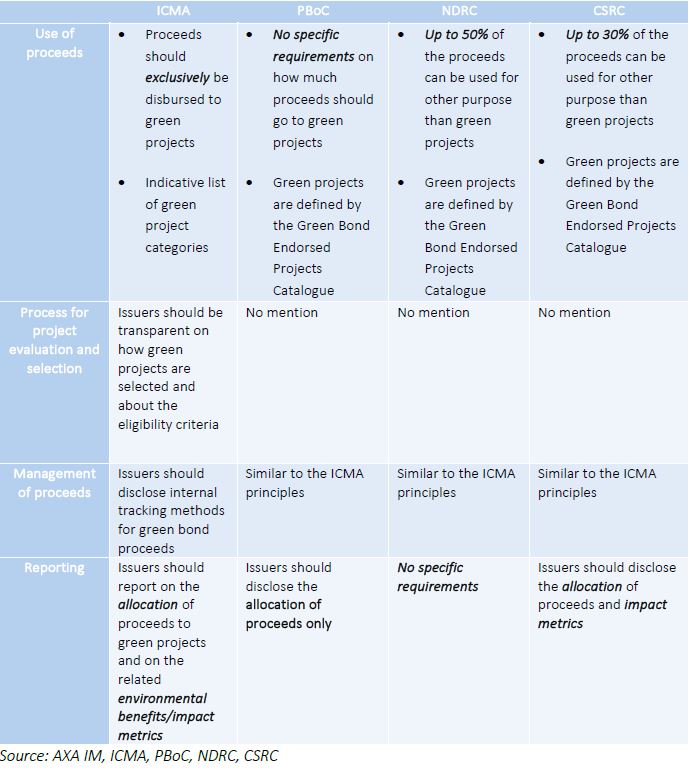

Discrepancies between Chinese and global green bond standards

Green bonds are usually governed by guidelines, notably those defined by the International Capital Markets Association (ICMA) and its Green Bond Principles4 . These are “voluntary process guidelines that recommend transparency and disclosure and promote integrity in the development of the green bond market by clarifying the approach for issuance of a green bond”.

The principles are based on four components: Use of proceeds; process for project evaluation and selection; management of proceeds and reporting.

It is also worth mentioning the Climate Bonds Initiative (CBI) standard, which is inspired by the principles, as well as the upcoming European Union Green Bond Standard which is very likely to be based on components of the same. At AXA IM, we have integrated these principles within our internal green bond assessment framework. All in all, the principles have played a crucial role in the development of the green bond market, and the bulk of green bond issuers align with them when coming to the market.

In China, however, green bonds guidelines differ depending on the type of issuer:

- Financial green bonds – from policy banks and financial institutions which follow the People’s Bank of China’s (PBoC) rules

- Enterprise green bonds – from state-owned companies that follow the National Development and Reform Commission’s (NDRC) rules

- Corporate green bonds – from private listed companies which adhere to the China Securities Regulatory Commission (CSRC) rules

As highlighted in Figure 2, when we compare the ICMA’s principles with the various regulations in China, we see many significant differences in terms of requirements and expectations for issuers. In our view, this can lead to confusion amongst market participants, and this is why we are calling for a harmonisation of Chinese and global green bond standards. Discussions have already started between market players, and AXA IM has been a part of that process – and we will of course continue to play our part in helping to harmonise green bond practices across geographies.

Figure 2: Comparison of Chinese green bond standards with the ICMA principles

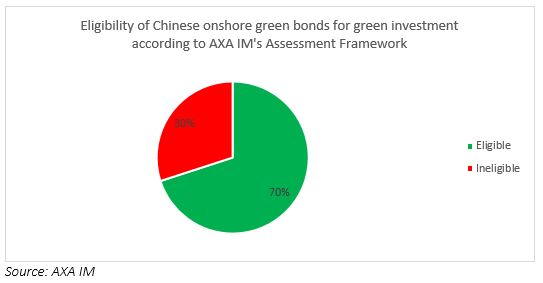

Beyond discrepancies in green bonds guidelines, there is another key difference we have observed in China’s market, around transparency and dialogue between issuers and investors. We evaluated 20 Chinese onshore green bonds against AXA IM’s internal criteria. For none of these have we been given the chance to interact directly with the issuer – either before or after issuance. We also have seen that Chinese issuers rarely conduct roadshow exercises, which reduces the ability for green bond investors to engage with them. Looking globally, we met with around 70% of the green bonds issuers assessed.

We believe that a direct dialogue with issuers allows us to dig deep into their sustainability ambitions and green bond frameworks and so it is key to ensure that our analysis is comprehensive and not compromised by disclosure issues. This is the main reason behind our second call – investors must pursue improved transparency and better dialogue with Chinese green bond issuers.

Chinese onshore green bonds and AXA IM’s assessment framework

As part of efforts to drive improvements in the green bond industry, AXA IM developed a proprietary assessment framework for green bonds. This integrates the components of the ICMA Green Bond Principles, and is based around the following pillars:

- The ESG quality and strategy and the issuer

- The use of proceeds and process for project selection

- The management of proceeds

- Impact reporting

Despite the differences in terms of green bond standards and practices between the Chinese onshore and global green bond market, we have decided to stick to our rigorous assessment criteria for Chinese onshore green bonds. Regardless of issuers’ sectors or geographies, we want to invest only in high-quality, impactful green bonds. The analysis we conducted on Chinese onshore green bonds highlighted aspects where we see room for improvement for issuers – in particular on the first, second and fourth pillars of our assessment framework.

Figure 3: Refining the universe of Chinese Green Bonds

Seeking improvements in ESG strategy and sustainability ambitions

We expect green bond issuers to align their overall business model with the goals of the Paris Agreement on climate change and a global warming scenario below +2°C of pre-industrial times. Having insights about issuers’ climate change strategy is key for us to better understand the consistency and the rationale behind issuing a green bond. For Chinese onshore green bond issuers, only four out of the 16 we analysed established clear forward-looking objectives aimed at reducing their environmental footprint.

This does not mean that we rush to exclude their green bonds, but we urge Chinese issuers to set and disclose clear climate strategies, and establish related forward-looking targets. This would only strengthen the rationale and the message behind Chinese onshore green bonds. We also believe that Chinese issuers need to set ambitious climate targets to demonstrate they will play their part in achieving China’s 2060 net-zero commitment. This is at the heart of our call for the establishment and disclosure of a clear sustainability strategy and objectives from Chinese green bond issuers.

Use of proceeds and process for project selection

The differences in green taxonomies do not make it impossible for us to identify the type of green projects and their quality for Chinese onshore green bonds. We have found that the level of transparency is generally high enough on the green assets that will be financed. We nevertheless expect a bit more colour around the eligibility criteria for green projects from Chinese issuers.

The biggest issue we see on the use of proceeds issue lies around the requirements for the share of proceeds that must go to green projects, as highlighted in Figure 2. We systematically excluded from our green investments the Chinese onshore green bonds for which less than 100% of the proceeds are earmarked for green assets. One of our key eligibility criteria for green bonds is that issuers commit to use the totality of the proceeds to finance green projects, as defined within their frameworks.

Impact reporting

We also expect green bond issuers to publish impact reports and to provide investors with impact metrics related to the funded projects. Once again, and as shown in Figure 2, standards on reporting for Chinese onshore green bonds differ depending on the type of issuer, which can raise issues when it comes to AXA IM’s green bond assessment framework – even though the ICMA principles do not require but only encourage impact reporting.

That being said, we were happy to see that most of the Chinese onshore green bonds we reviewed did provide impact metrics – generally in the pre-issuance documentation. Still, the absence of a commitment to provide impact reporting was a key reason to exclude three Chinese onshore green bonds out of the 20 we reviewed from our green investments.

Our ambitions for Chinese onshore green bonds

While we have highlighted areas of improvement for Chinese onshore green bond issuers, this should be taken as advice and feedback to issuers rather than criticism. At AXA IM, we are convinced that Chinese onshore green bonds represent a major opportunity with regards to our climate ambitions. Even if these only represent a tiny part of our overall green bond investments at the moment, we are willing to become a significant investor in the Chinese green bond market.

As described above, we believe that harmonising Chinese and global green bond standards, while improving dialogue and transparency between Chinese green bond issuers and investors, will help us to achieve our ambitions. This will also be helped by Chinese issuers setting and disclosing clear sustainability strategies and objectives. We continue to pursue a leadership role in the green bonds sector and will bolster our engagement with the stakeholders of the Chinese onshore green bond market as we seek to ensure it will evolve in the right direction – as it has already started to do.

- IGh0dHBzOi8vd3d3LmF4YS1pbS5jb20vY29udGVudC8tL2Fzc2V0X3B1Ymxpc2hlci9hbHBlWEtrMWdrMk4vY29udGVudC9heGEtaW0tcmVhY2hlcy1lMi04Mi1hYzEzYm4tbWlsZXN0b25lLWluLWdyZWVuLXNvY2lhbC1hbmQtc3VzdGFpbmFiaWxpdHktYm9uZHMtYW5kLXVudmVpbHMtYS1zdHJlbmd0aGVuZWQtZnJhbWV3b3JrLXRvLWFzc2Vzcy1zdWNoLWludmVzdG1lbnRzLzIzODE4

- aHR0cHM6Ly93d3cuYXhhLWltLmNvbS9kb2N1bWVudHMvMjAxOTUvODU5MjM2L0NoaW5hKy0rRmluYW5jaW5nK3RoZStHcmVlbit0cmFuc2Zvcm1hdGlvbisyMDIxMDQyOStlbi5wZGYvZjc3ZDFiOTUtMDg1ZC0yN2U3LTk2M2QtNDJkMTg5NzVmNzk4P3Q9MTYxOTY4MTU4NDU5OQ==

- aHR0cHM6Ly93d3cuYXhhLWltLmNvbS9kb2N1bWVudHMvMjAxOTUvNjA3NDgyL0dyZWVuK0JvbmRzK0ZyYW1ld29yay1pbnRlcmFjdGlmLnBkZi8zNWZhZTZlZi0yYjI0LTdiNGMtZmNiYy02MzJlNjJlZjkzNTY/dD0xNjIwMTQ1OTY4ODI5

- aHR0cHM6Ly93d3cuaWNtYWdyb3VwLm9yZy9hc3NldHMvZG9jdW1lbnRzL1JlZ3VsYXRvcnkvR3JlZW4tQm9uZHMvR3JlZW4tQm9uZHMtUHJpbmNpcGxlcy1KdW5lLTIwMTgtMjcwNTIwLnBkZiA=

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2021 AXA Investment Managers. All rights reserved