How the younger generations’ new priorities shape investment opportunities

As Generation Z comes of age, soon followed by Generation Alpha, their priorities and preferences could reshape parts of the economy and lead investors to substantial returns.

The U.S. population has been aging, giving rise to a burgeoning Silver Economy, with the 65-plus population experiencing a growth rate of 38.6% for the largest-ever 10-year gain between 2010 and 2020.

Gen Z, those born between approximately 1995 and 2010 (and our main focus), already comprises about 21% of the U.S. population.

As Gen Z joins Millennials and enters the workforce, the U.S. economy will likely experience higher consumption, wages, and housing demand, leading to a higher GDP, and providing a better outlook for Social Security and Medicare programs, as well as the potential for notable ROIs for today’s investors as these trends come to fruition.

Financial priorities as younger generations enter adulthood

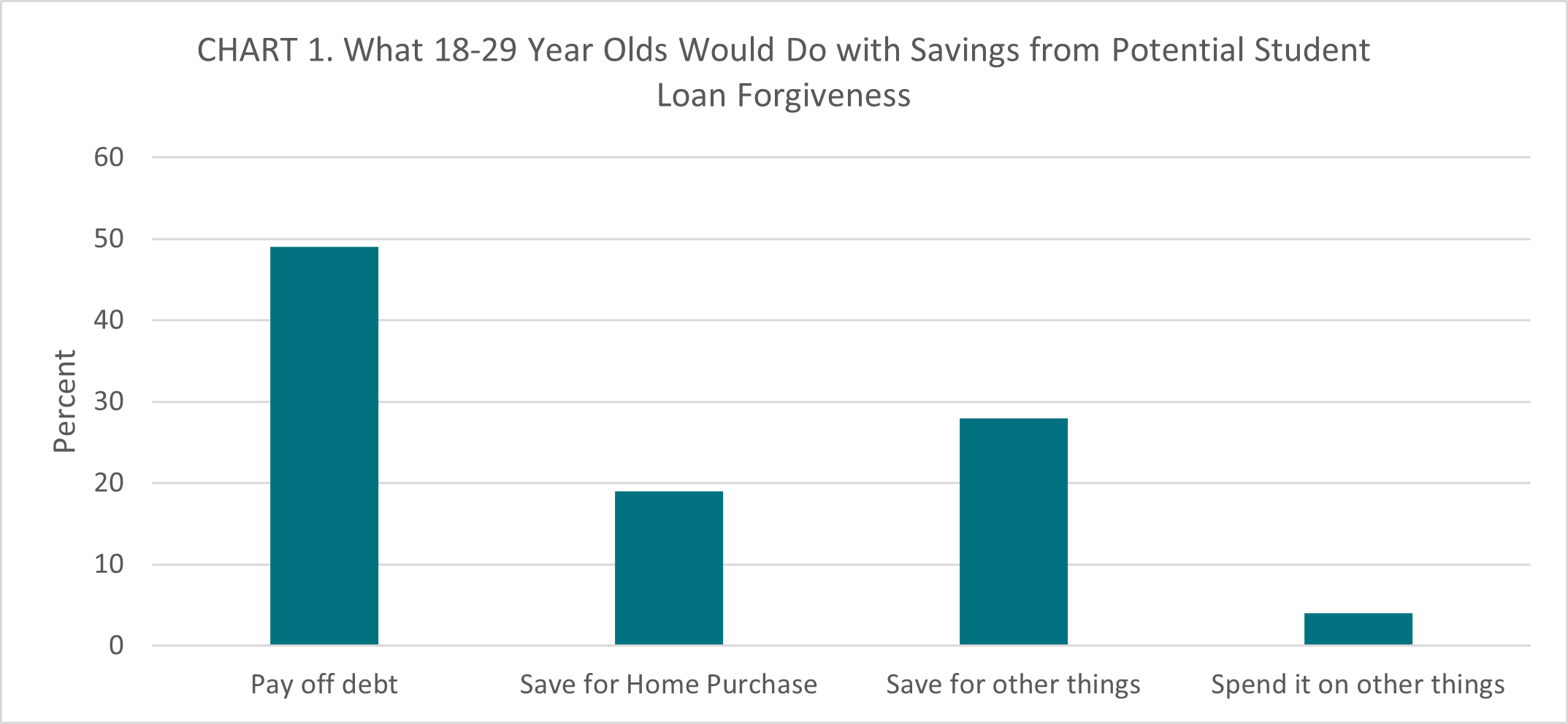

While the burden of student loans has hindered the economic power of Millennials, Gen Z is paving a different path, with many opting for shorter, more affordable direct-to-career pathways to avoid student loans.

According to Federal Reserve data, 47% of all student loan holders owe at least $25,000 of debt.

Source: Haver Analytics, Federal Reserve, Rosenberg Research (United States: Economic Well-Being of U.S. Households)

At the same time, Gen Z’s income is growing and is expected to increase fivefold by 2030 – reaching $33 trillion – accounting for more than a quarter of global income and surpassing Millennials’ pay by 2031.

A recent report found that 46% of members in Gen Z above the age of 18 have a side job.

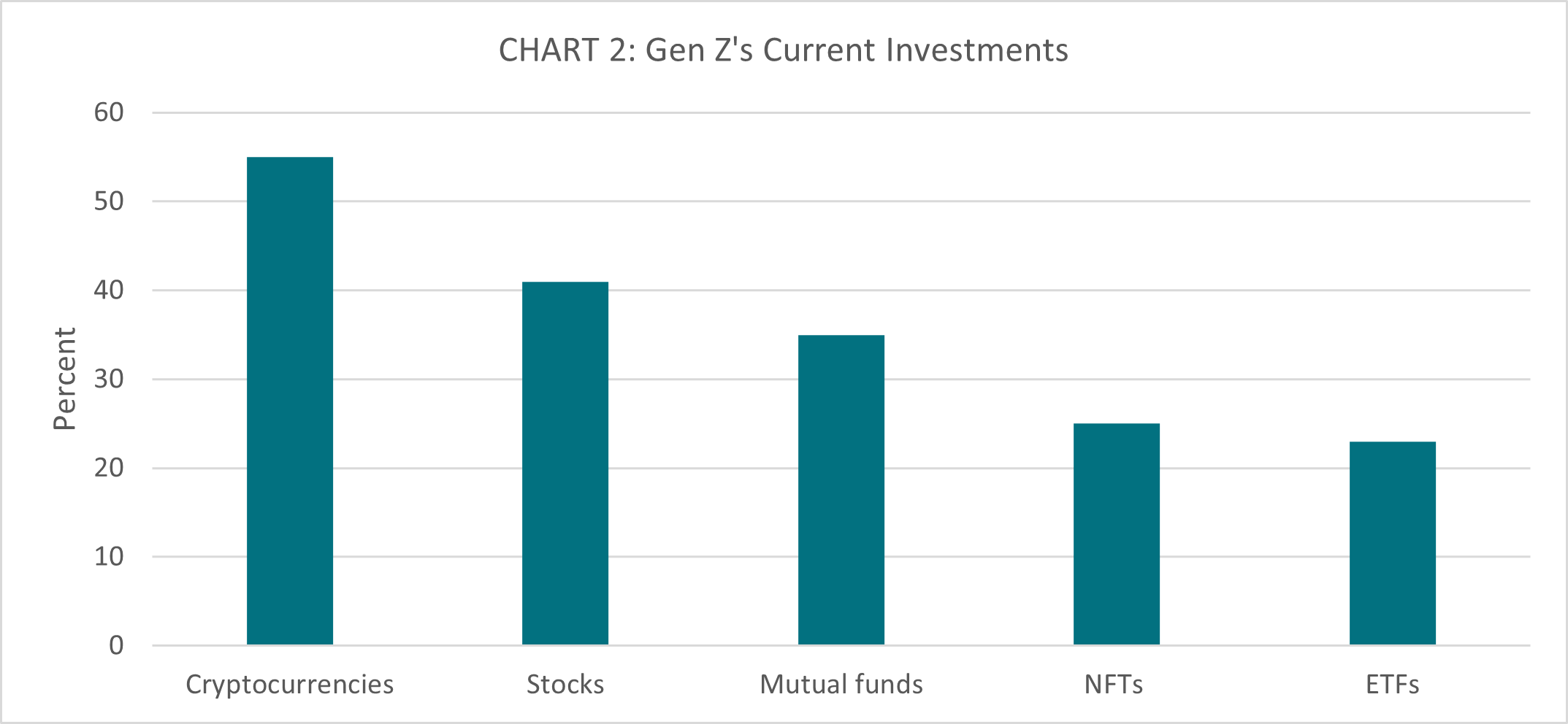

While Gen Z is often maligned for poor savings habits, members of this generation have in fact made impressive strides in taking hold of their own portfolios. A full 56% of Gen Z owns at least some investments, and 15% started investing before the age of 18.

The long term winners from this trend will be the platform providers who captured the Gen Z market by offering “micro finance” investments, as67% of Gen Z investors say they started because they were able to start with small amounts.

Source: Haver Analytics, CFA, Rosenberg Research (Gen Z and Investing: social media, Crypto, FOMO, and Family)

Source: Haver Analytics, CFA, Rosenberg Research (Gen Z and Investing: social media, Crypto, FOMO, and Family)

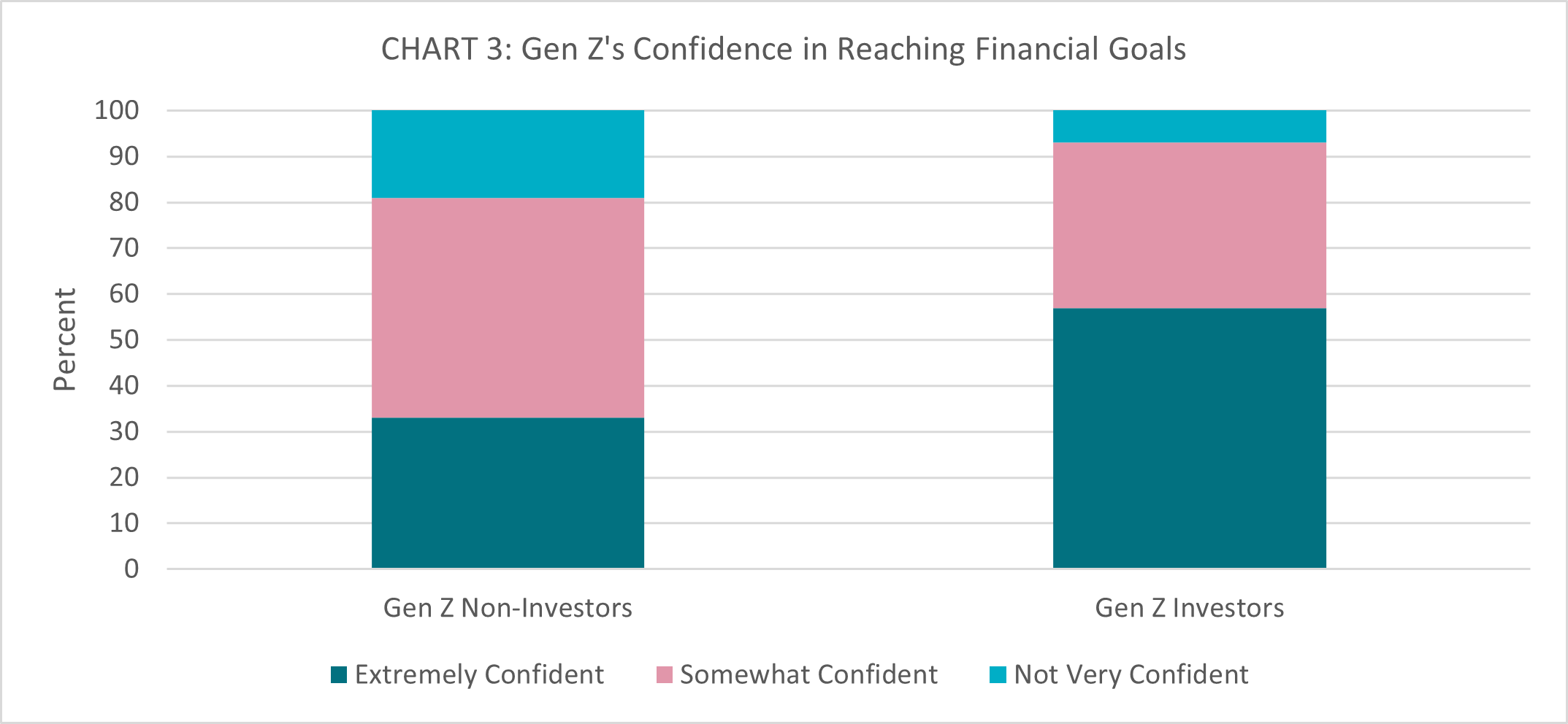

The upshot is that Gen Z is actually ahead of the curve on retirement savings, with 62% of Gen Zers participating in 401(k)s or similar retirement savings plans.

Furthermore, younger generations stand to gain from the Great Wealth Transfer. Notably, the wealth amassed by the U.S. Baby Boomers and the Silent Generation, totaling $78 trillion, is expected to be passed on to their descendants, raising their purchasing power.

Though continued inflation and soaring mortgage rates have reshaped this landscape more recently, Gen Zers’ saving habits and the low mortgage rates brought on by the COVID-19 pandemic have them tracking ahead of Millennials and Gen Xers when it comes to homeownership, with nearly 30% of 25-year-olds owning their own homes.

Gen Z and Gen Alpha as tech-focused, ethical consumers

Gen Z is proving to be exceptionally financially savvy, which could lead to an increase in purchasing power. This trend not only creates opportunities for businesses aligned with Gen Z’s preferences to thrive but also offers a potentially profitable avenue for investors to explore. Gen Alpha is too young to spend today, but as they become teenagers and young adults, their purchasing power will rise quickly.

Looking at these young generations, the most notable areas that can potentially generate sustainable stakeholder value include:

- Technology: As the first generation to be fully digital natives, technology is foundational to Gen Z. Social media usage amongst this generation is high. 95% of Gen Zers are on YouTube, 67% are on TikTok, and 62% are on Instagram.

Pew Research Center (8/10/2022): Teens, Social Media and Technology 2022 The average member of Gen Z spends an average of 3.4 hours per day streaming videos.Exploding Topics (2/15/2023): 7 Key Gen Z Trends for 2023 Statista (6/27/2023): Frequency of online shopping among Gen Z consumers in the United States in 1st quarter 2023 Meanwhile, Gen Alpha is growing up in a different world, shaped by AIInsider Intelligence (2/7/2023): Gen Alpha will be more diverse than the rest of the US population . While the usage of screens from young ages could have developmental impacts – something parents, educators, legislators, and investors alike will be closely monitoring – technology’s prevalence and early adoption in this demographic will increase their digital literacy and appetite for digital solutions.

One trend that is widely popular with Gen Zers is buy now, pay later (BNPL) services. More than 44% of Gen Z have used a BNPL service at least once in 2022.

- Companies that provide access: While older generations prioritized ownership, Gen Z views consumption a little differently. For Gen Zers, consumption is about having access to products and services, which is why services like Uber, Lyft, bike shares, and streaming services like Netflix, Hulu, and Spotify are so popular and could present investment opportunities.

McKinsey (11/12/2018): ‘True Gen’: Generation Z and its implications for companies For Gen Alpha, the sharing and streaming economy will likely remain popular because it’s all they’ve ever known when it comes to consuming entertainment. - Personalization: Gen Z isn’t afraid to spend more for what they want and will choose quality over price, but they aren’t specifically after luxury, name-brand products.

McKinsey (8/4/2020): Meet Generation Z: Shaping the future of shopping Instead, as the most diverse generation (until Gen Alpha comes of age), they consider consumption an expression of individual identity, meaning investing in companies that create personalized products reflective of Gen Zers is promising. So, it’s hardly surprising that Nike has introduced Nike By You, a co-creation service that allows customers to personalize and design their shoes. Similarly, Function of Beauty enables shoppers to create custom shampoo, conditioner, and body wash. - Ethics and sustainability: Compared to previous generations, Gen Z shoppers are likelier to view consumption through an ethical lens, with 65% wanting to learn the origins of their purchases and 80% refusing to buy from companies involved in scandals.

McKinsey (11/12/2018): ‘True Gen’: Generation Z and its implications for companies Gen Z’s ethical concerns also extend to sustainability, as three-quarters of Gen Zers rank sustainability’s importance higher than brand name.Forbes (2/18/2022): Gen Z And Sustainability: The Disruption Has Only Just Begun In fact, most members of Gen Z are willing to spend 10% more on sustainable products.NASDAQ (9/23/2022): How Millennials and Gen Z Are Driving Growth Behind ESG There’s reason to believe this trend with continue with Gen Alpha, as they are growing up with unparalleled exposure to information about social issues and world events.

Consumption habits of Gen Z

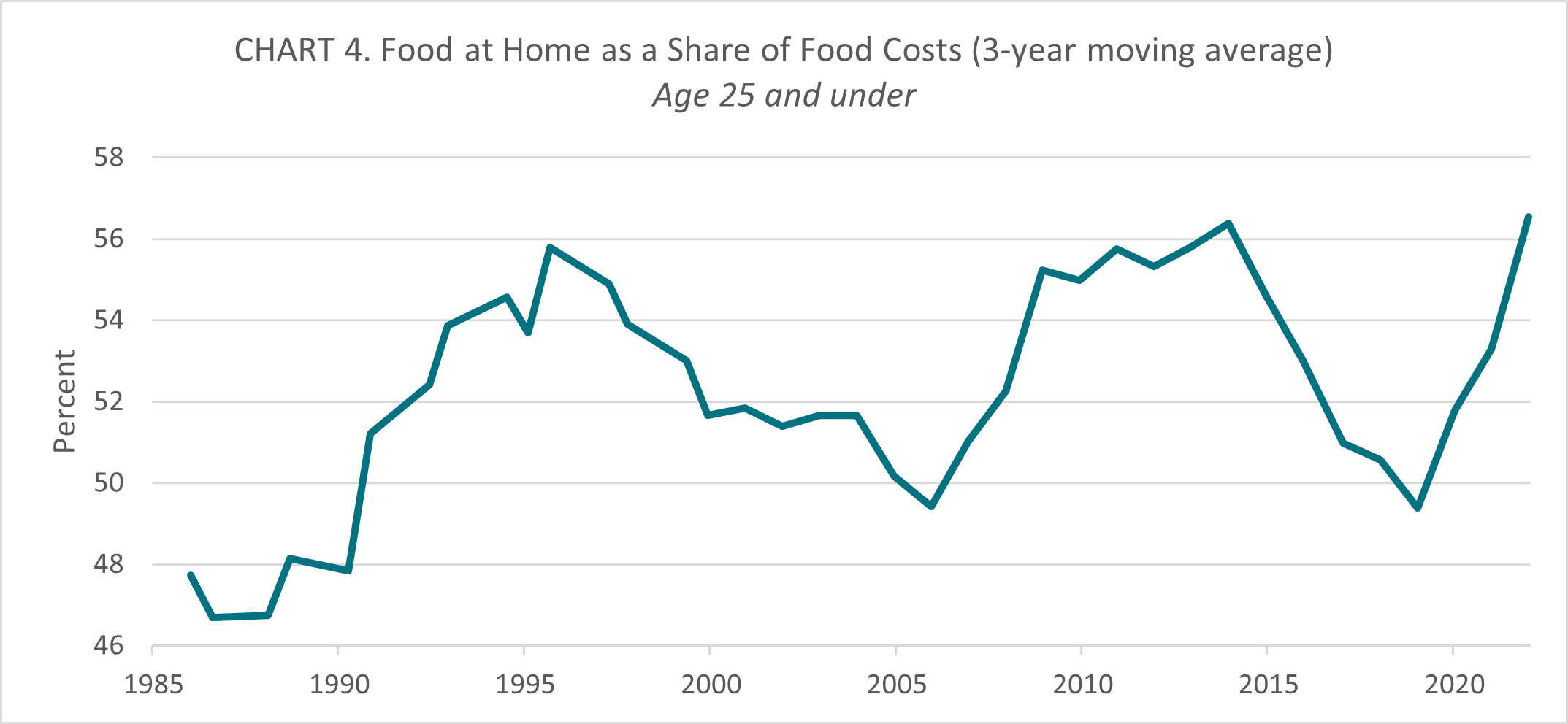

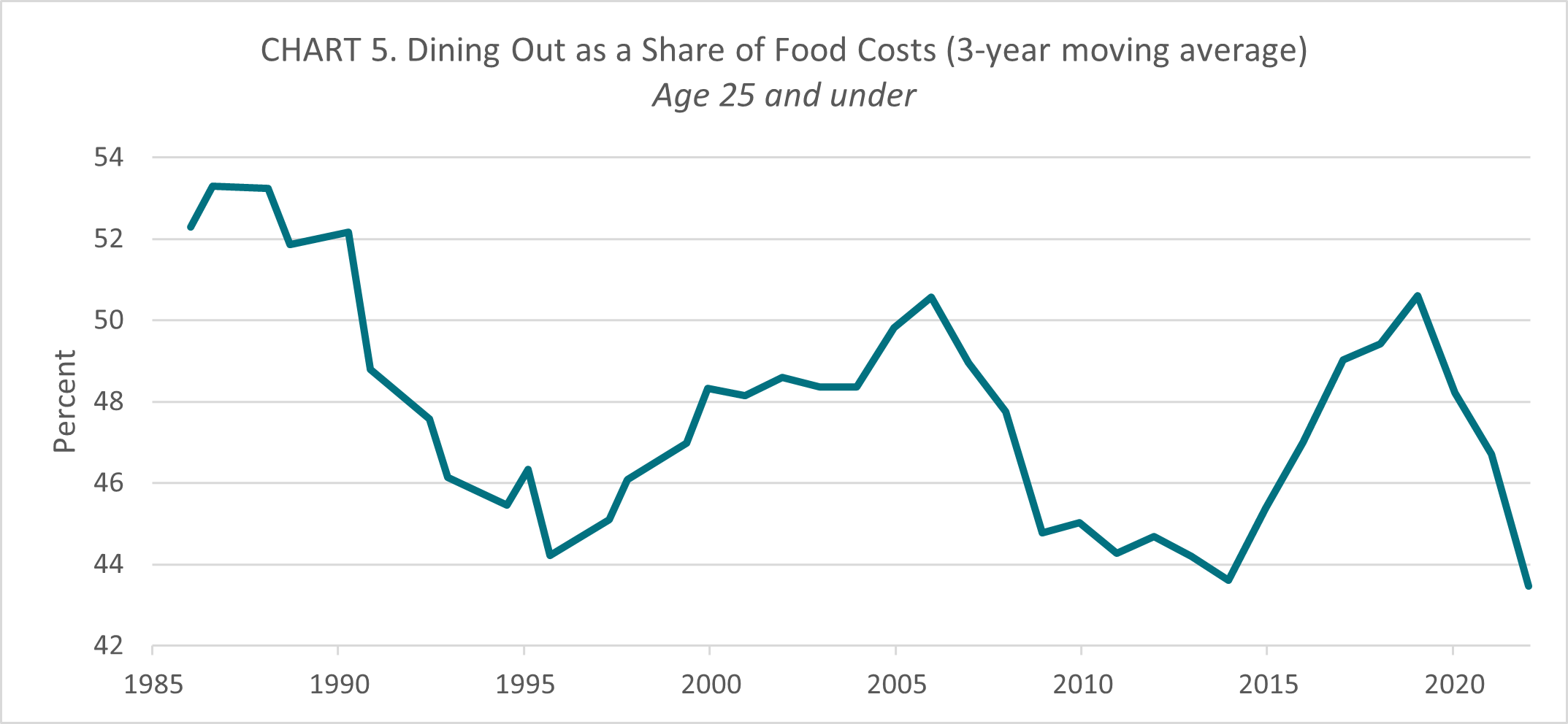

Since COVID-19 there has been a shift in Gen Z’s consumption habits, relating in particular to basic retail categories such as food and apparel. Gen Z is leading the broad shift from dining out to eating in, as cost-consciousness rises and COVID-19 habits persist.

Federal Reserve of New York (n.d.): Household Debt and Credit Report

Source: Haver Analytics, BLS, Rosenberg Research, (Consumer Expenditure Survey)

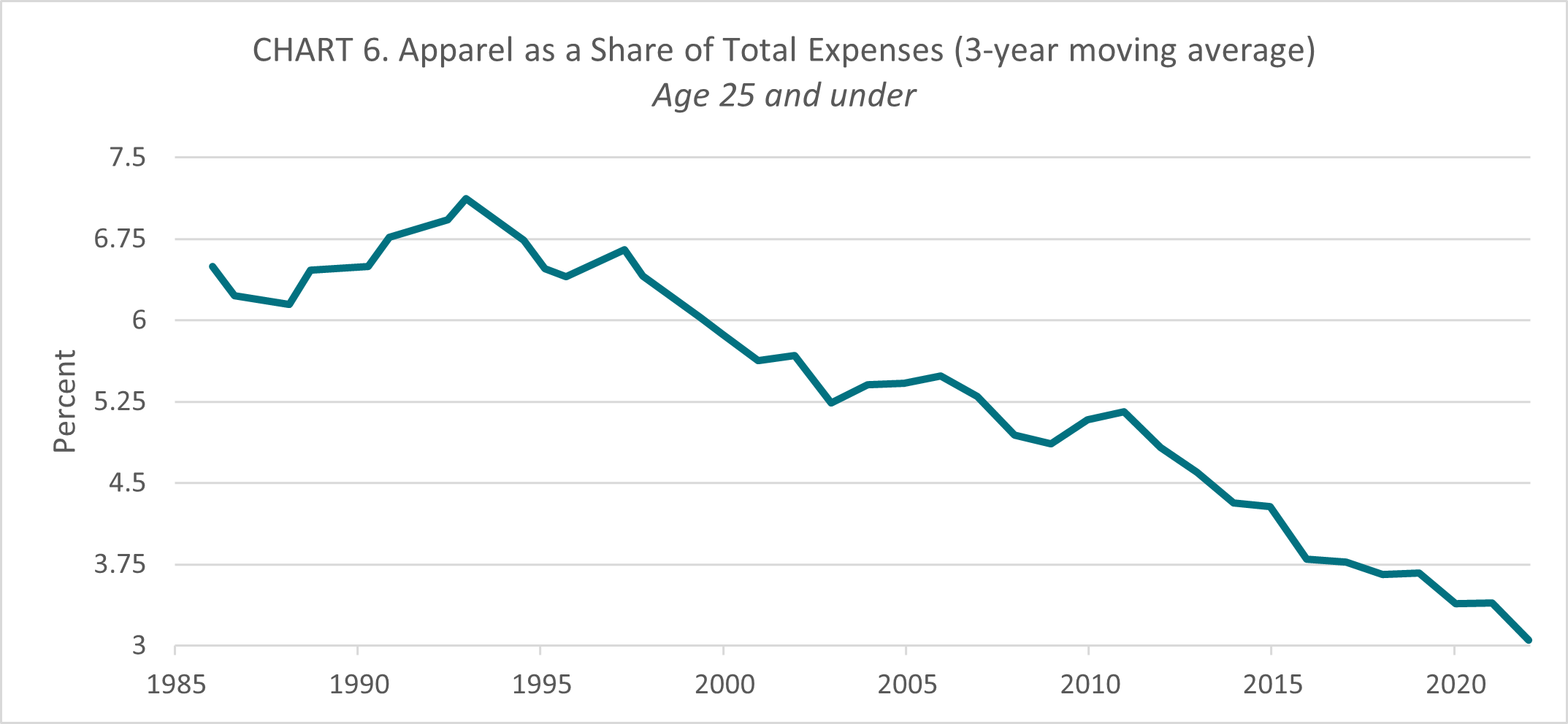

The amount young people spend on apparel as a share of total expenses has been declining since the 1990s, and 27% of this generation is more likely to shop secondhand.

Source: Haver Analytics, BLS, Rosenberg Research, (Consumer Expenditure Survey)

A new generation rises up and has the potential to reshape the economy

The Silent Generation and Baby Boomers are slowly making their exit and losing their purchasing power, leaving room for Gen Z, which is set to become the largest cohort in the U.S. in around a decade, as well as the growing Gen Alpha, to potentially drive a Youth Boom Economy. Companies that can pivot to cater to these younger generations’ needs may benefit financially, and investors can actually seek to reduce risk and increase their returns by paying attention to companies focusing on these youthful demographics.

Risk Warning:

Investment involves risk including the loss of capital.

Our experts and investment teams outline their key convictions

Visit the Investment InstituteDisclaimer

This document is being provided for informational purposes only. The information contained herein is confidential and is intended solely for the person to which it has been delivered. It may not be reproduced or transmitted, in whole or in part, by any means, to third parties without the prior consent of the AXA Investment Managers, Inc. (the “Adviser”). This communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

© 2023 AXA Investment Managers. All rights reserved

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.