It’s raining again

Like the British weather, markets in August can often be disappointing. A US ratings downgrade, concerns about supply, and an acceptance that there will be limited interest rate relief in a ‘soft landing’ scenario have conspired to push US Treasury yields back towards their highest levels since October. At the same time, the second quarter (Q2) earnings season has been in line with expectations, but the reality is earnings are some 8% lower than they were a year ago. Valuations are adjusting to both the ‘higher for longer’ interest rate outlook and the more challenging environment for corporate profit margins. Worrying climatic events, a toxic US political environment and thin liquidity conditions aren’t helping. Some investors may well be on the beach after having banked the profits following the market rally of recent months. After the summer, bonds should look attractive, especially with lower inflation, but Q3’s seasonal market reports are mixed at the best of times. Like taking an umbrella to the beach, cash might still be the best choice in an uncertain market environment.

Summer jobs

In recent weeks I have discussed how the soft landing scenario for the US economy has increasingly dominated how markets have performed. The falling probability of a near-term recession means equities have outperformed fixed income. Despite bond markets being a more lucrative source of income than they have been for many years - because of higher yields - the long-duration trade driven by an expectation of slowing growth and inflation and eventual monetary easing has not worked. The macro data has supported the growth view. Yes, some indicators, like the Institute for Supply Management’s (ISM) manufacturing conditions index have been weak, but the labour market remains strong. Our quantitative equities team did some work, using Natural Language Processing, examining whether there has been any increase in references to lay-offs in corporate earnings statements this year (or similar language indicating deteriorating employment conditions). The research did indicate some rise compared to 2022, but not anything alarming. It was mostly confined to sectors like financial services and healthcare. Equally there has been an increase in the use of the word “hiring” in sectors like software. The hard data too, suggests the US labour market remains strong which should support consumer spending in the immediate future.

But August can be the cruellest month

Despite this, the beginning of August has seen some negative market moves. The decision by Fitch, the credit rating agency, to downgrade the US came after the market had already become concerned about increased supply. The US Treasury has announced large increases in planned bond issuance. That, combined with upward revisions to growth over the next few quarters, and little scope for the Federal Reserve (Fed) to cut interest rates, might mean a higher equilibrium long-term bond yield is required. Whether it is higher yields or not, equities have also slipped at the start of this month. In aggregate, Q2 earnings numbers have not been that bad and have generally surprised to the upside (with more than 400 companies in the S&P 500 universe having reported at the time of writing). Earnings growth is around 8% lower compared to a year ago – driven by some negative outcomes in materials, the energy sector and healthcare. These are sectors that benefitted from specific developments in the last couple of years (higher energy prices, post-pandemic trends in drug development and treatments). However, some corporate reports have been at odds with the slower economic data. Industrials, consumer staples and discretionary and the communication services sector posted positive year-on-year growth in both revenues and earnings. Caterpillar, for example, reported earnings that were much stronger than macro indicators, like the ISM, would suggest. Technology results have been mostly positive with Amazon’s and Apple’s numbers on cloud computing reflecting the increased take-up of artificial intelligence applications.

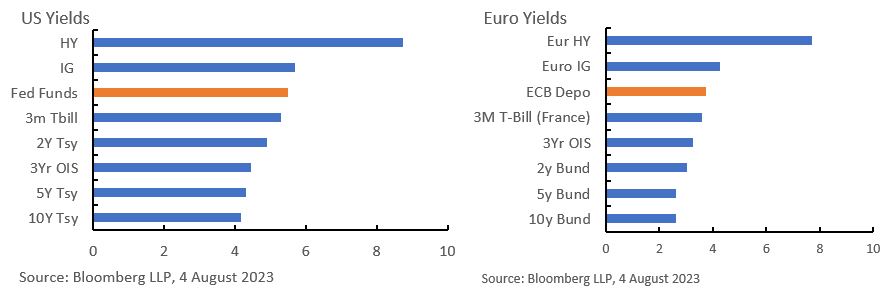

Skinny credit premium over cash

The interest rate environment makes it tough for investors. In both the US and the European fixed income markets, only the sub-investment grade markets yield materially higher than the overnight policy rate. The yield on representative investment-grade corporate bond indices is slightly above the policy rate. However, before the recent bond sell-off credit was at similar levels – something which is quite uncommon as the corporate bond market should offer a richer risk premium relative to the risk-free rate. In any risk-off environment it would make sense to keep money in short-term low-risk assets like Treasury bills than getting a similar yield in an asset class with both more credit and duration risk. Cash remains king for now.

Monetary policy might be more of a permanent headwind for markets

All the major central banks are saying the same thing. They have taken monetary policy into restrictive territory but need to continue to monitor whether conditions are tight enough to further reduce inflationary pressures. At best, this means policy is on hold for some time, because it will take some time for inflation to return to central bank target levels. At worst, it could mean even higher rates if something comes along to push inflation back up.

One thing investors now need to consider is whether we are in a permanently higher or more volatile inflationary environment. If inflation periodically exceeds central bank target ranges, then more frequent monetary policy changes might be needed in the future. That requires a greater uncertainty premium in forward rate curves (the term premium) and higher yields than would be the case if inflation was to stabilise within central bank tolerance ranges. This may be another reason why longer-term yields are failing to move lower and yield curves have started to steepen. I must admit, the rise in yields has been a surprise given the inflation and Fed outlook backdrop. Yet fundamentally it might make sense, particularly given the deterioration in the government’s borrowing outlook.

The good thing about this move is that yields on credit have moved higher again. Yes, they are hardly above the overnight policy rate. But short rates won’t stay this high permanently and for those with an investment horizon that stretches beyond the next six to 12 months, the implied income return from the investment growth bond market is more attractive now than it has been for most of the last decade. It also remains the case that a good portion of the bond market – at all levels of credit risk – continues to trade with prices well below par. Short-term volatility notwithstanding, there continues to be interesting opportunities in fixed income.

Cruel summer in blighty

This is nowhere more evident than in the UK with longer-dated gilts trading on very low prices. The potential upside is considerable once the interest rate cycle changes. The Bank of England raised rates to 5.25% this week and like its peers, the suggestion was the peak in rates will be in place for some time. The main concern seems to be around wage growth in an economy that continues to struggle with labour supply. Interest rates are a blunt instrument – monetary policy can’t conjure up new workers - and broader government policy does not seem to be able to deal with these issues (suggesting that over 50s who may have lost their jobs consider becoming bartenders or food delivery operatives is not likely to be a realistic or politically appealing way to deal with structural labour market concerns). My view is the UK will start to really suffer from higher interest rates, with house prices already starting to crack and sentiment around household incomes weakening quickly. Companies won’t be paying higher wages if there is no-one to buy their goods and services. Gilts look good value from the perspective of where the UK economy seems to be heading.

The heat and the rain

This summer has certainly provided more evidence of the economic risks from climate change. There have been extreme temperatures in numerous parts of the world, violent storms generating heavy rainfall and flooding, and unseasonably cold and wet conditions. The economic damage is clear – wildfires impacting on tourism in numerous places in the Mediterranean, flooding affecting travel in China, and agricultural output at risk in many places. Moreover, oil and gasoline prices have been rising again reflecting OPEC’s supply restrictions and some issues at refineries and storage facilities for refined products. In the US, average gasoline prices increased around 5.6% per gallon during July. The end impact on consumer price inflation might be limited by this summer’s events but they serve to remind us why climate change mitigation, shifting to a more manageable energy system and risk management around climate are all so important.

Holidays in the sun (🤞)

I’m going to take a week off so there will be no note from me next week. It’s not an overstatement to say that it has not been a great summer in the UK in terms of weather. There has been a lot of rain. Thankfully, Wimbledon and the Ashes cricket series were not too badly impacted (although the weather stopped England from winning the series against Australia, which would have meant regaining the Ashes). Never mind, the England cricket team get another chance in 18 months’ time down under. I am hoping the weather improves over the rest of August and lets me do some walking in Cornwall. Before you know it, it will be the start of the football season. My sanity will again be tested by Manchester United. Can’t wait! Meanwhile enjoy the holidays.

(Performance data/data sources: Refinitiv Datastream, Bloomberg). Past performance should not be seen as a guide to future returns.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2023 AXA Investment Managers. All rights reserved

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.